1.기업개요

About KB Home

KB Home is one of the largest and most recognized homebuilders in the United States and has built over 655,000 quality homes in our 65-year history. Today, KB Home operates in 47 markets from coast to coast. What sets KB Home apart is the exceptional personalization we offer our homebuyers—from those buying their first home to experienced buyers—allowing them to make their home uniquely their own, at a price that fits their budget. As the leader in energy-efficient homebuilding, KB Home was the first builder to make every home it builds ENERGY STAR® certified, a standard of energy performance achieved by fewer than 10% of new homes in America, and has built more ENERGY STAR certified homes than any other builder. An energy-efficient KB home helps lower the cost of ownership and is designed to be healthier, more comfortable and better for the environment than new homes without certification. We build strong, personal relationships with our customers so they have a real partner in the homebuying process. As a result, we have the distinction of being the #1 customer-ranked national homebuilder in third-party buyer satisfaction surveys.

KB Home은 미국에서 가장 크고 가장 인정받는 주택 건설업체 중 하나이며 65년의 역사 동안 655,000채 이상의 고급 주택을 건설했습니다. 현재 KB홈은 전국 47개 시장에서 사업을 펼치고 있습니다. KB Home을 차별화하는 점은 첫 주택을 구입하는 사람부터 경험 많은 구매자에 이르기까지 주택 구입자들에게 예산에 맞는 가격으로 자신의 집을 독특하게 만들 수 있도록 하는 탁월한 개인화입니다.

KB Home은 에너지 효율적인 주택 건설의 선두 업체로서, 미국 내 10% 미만의 신규 주택이 달성한 에너지 성능 기준인 ENERGY STAR® 인증을 받은 모든 주택을 최초로 건설했으며, 다른 어떤 건설업체보다 더 많은 ENERGY STAR 인증 주택을 건설했습니다. 에너지 효율적인 KB 주택은 소유 비용을 절감하는 데 도움이 되며 인증 이 없는 새 주택보다 건강하고 편안하며 환경에 더 적합하도록 설계되었습니다. 우리는 고객과 강력하고 개인적인 관계를 구축하여 고객이 주택 구입 과정에서 진정한 파트너를 가질 수 있도록 합니다. 그 결과, 우리는 제3자 구매자 만족도 조사에서 고객 랭킹 1위 주택 건설업체로 선정 되었습니다.

2.실적리뷰

실적을 리뷰하기전에 KB홈의 CEO인 Jeffrey Mezger의 발언을 보고 가겠습니다.

“We delivered strong results in the second quarter, generating significant year-over-year growth in revenues, operating income and diluted earnings per share,” said Jeffrey Mezger, Chairman, President and Chief Executive Officer. “With our ending backlog of over $6 billion, we are reaffirming our fiscal 2022 guidance, which we believe we are well positioned to achieve.”

우리는 2분기에 매출, 영업 이익 및 희석 주당 이익에서 상당한 전년 대비 성장을 달성하면서 강력한 결과를 제공했습니다. 60억 달러가 넘는 최종 잔고와 함께 우리는 달성하기에 좋은 위치에 있다고 생각하는 2022 회계연도 가이던스를 재확인 합니다.

“Sales rates are moderating from the exceptional levels the industry has experienced, as buyers process the impact of higher mortgage interest rates, as well as inflationary pressures. We believe the flexibility of our Built-to-Order business model will enable us to navigate these changing market conditions. Our model allows our customers to choose from a wide array of floorplans and price points, offering them the ability to personalize their home in a way that reflects what they value and can afford. Our approach resonates with buyers and is a key reason we have sustained among the highest absorption rates in the industry for many years.”

구매자가 높은 모기지 이자율과 인플레이션 압력의 영향을 처리함에 따라 판매율은 업계가 경험한 예외적인 수준에서 완화되고 있습니다. 우리는 주문 생산 방식의 비즈니스 모델의 유연성이 이러한 변화하는 시장 상황을 헤쳐나갈 수 있게 해줄 것이라고 믿습니다. 우리 모델은 고객들이 다양한 평면도와 가격대에서 선택할 수 있도록 하여 그들이 가치 있고 감당할 수 있는 것을 반영하는 방식으로 집을 개인화할 수 있는 능력을 제공합니다. 우리의 접근 방식은 구매자들에게 큰 반향을 불러일으키며, 우리가 수년 동안 업계에서 가장 높은 흡수율을 유지해 온 주요 이유입니다.

“We will remain strategic in our capital allocation decisions to maximize returns in this environment. We currently own or control all of the lots we need to support our delivery targets through 2024. As a result, we are in a favorable position to calibrate our land investments to evolving conditions, without compromising our mid-term growth, providing us with opportunities to redeploy capital to stockholders,” concluded Mezger.

우리는 이러한 환경에서 수익을 극대화하기 위해 자본 할당 결정에 있어 전략적 위치를 유지할 것입니다. 우리는 현재 2024년까지 인도 목표를 지원하는 데 필요한 모든 부지를 소유하거나 통제하고 있습니다. 결과적으로, 우리는 우리의 중기 성장을 저해하지 않고, 우리의 토지 투자를 변화하는 상황에 맞게 조정하여 주주들에게 자본을 재배치할 수 있는 기회를 제공할 수 있는 유리한 위치에 있습니다.

매출 : 1.72B

예측 : 1.65B(+4.24%)

EPS : 2.32

예측 : 2.04(+13.73%)

Three Months Ended May 31, 2022 (comparisons on a year-over-year basis)

Revenues grew 19% to $1.72 billion.

Homes delivered were essentially even at 3,469.

Average selling price rose 21% to $494,300.

Homebuilding operating income grew 62% to $264.5 million. The homebuilding operating income margin increased 410 basis points to 15.4% as a result of improvements in both the housing gross profit margin and selling, general and administrative expense ratio.

The housing gross profit margin increased 390 basis points to 25.3%, reflecting a favorable pricing environment due to strong demand and the limited supply of homes available for sale, and lower relative amortization of previously capitalized interest. These positive impacts were partly offset by higher construction costs, including elevated lumber prices, and increased expenses to support current operations and expected growth.

Selling, general and administrative expenses as a percentage of housing revenues improved 30 basis points to 9.8%, primarily reflecting lower external sales commissions and increased operating leverage from higher revenues, partly offset by higher expenses to support growth.

The Company’s financial services operations generated pretax income of $18.7 million, up 75%, reflecting significant growth in the equity in income of its mortgage banking joint venture, KBHS Home Loans, LLC, as a result of an increase in interest rate lock commitments (“IRLCs”). The dollar volume and duration of IRLCs increased significantly during the quarter as more buyers locked their mortgage interest rates.

Total pretax income grew 63% to $282.9 million and, as a percentage of revenues, increased 430 basis points to 16.4%.

The Company’s income tax expense and effective tax rate were $72.2 million and approximately 26%, respectively, compared to $30.3 million and approximately 17%. The higher effective tax rate mainly reflected the expiration of federal tax credits for building energy-efficient homes delivered after December 31, 2021.

Net income of $210.7 million and diluted earnings per share of $2.32 increased 47% and 55%, respectively.

매출은 19% 증가한 17억2000만 달러를 기록했습니다.

인도된 주택은 기본적으로 3,469채였습니다.

평균 판매 가격은 $494,300로 21% 상승했습니다.

주택 건설 영업 이익은 62% 증가한 2억 6,450만 달러를 기록했습니다.

주택 건설 영업 이익률은 주택 총 이익 마진과 판매, 일반 및 관리 비용 비율이 모두 개선 된 결과 15.4 %로 410BP 증가했습니다.

주택 매출총이익률은 390BP 증가한 25.3%로, 강한 수요와 판매 가능한 주택의 제한된 공급으로 인한 유리한 가격 책정 환경, 이전에 자본화된 이자의 상대적 상각비 감소를 반영했습니다. 이러한 긍정적인 영향은 목재 가격 상승을 포함한 더 높 은 건설 비용과 현재 운영 및 예상 성장을 지원하기 위한 비용 증가로 부분적으로 상쇄되었습니다.

주택 매출에서 판매, 일반 및 관리 비용이 차지하는 비율은 30bp 개선된 9.8%로 외부 판매 수수료 감소와 매출 증가로 인한 운영 레버리지 증가를 반영하며, 성장 지원을 위한 비용 증가로 일부 상쇄되었습니다.

회사의 금융 서비스 운영은 이자율 고정 약정(IRLCs)의 증가로 인해 모기지 은행 합작 회사인 KBHS Home Loans, LLC의 소득에서 상당한 증가를 반영하여 75% 증가한 1,870만 달러의 세전 수익을 창출했습니다. IRLC의 달러 규모와 기간은 더 많은 구매자가 모기지 이자율을 고정함에 따라 분기 동안 크게 증가했습니다.

총 세전 이익은 63% 증가한 2억 8,290만 달러를 기록했으며, 매출 비율로 따지면 430bp 증가한 16.4%를 기록했습니다. 회사의 소득세 지출과 실효세율은 각각 7,220만 달러와 약 26%였으며, 전년동기 3,030만 달러와 약 17%와 비교됩니다. 더높은 실효 세율은 주로 2021년 12월 31일 이후 실행된 에너지 효율적인 주택 건설에 대한 연방 세금 공제의 만료를 반영했습니다.

2억 1070만 달러의 순이익과 2.32달러의 희석 주당 순이익은 각각 47%와 55% 증가했습니다.

Backlog and Net Orders (comparisons on a year-over-year basis)

Ending backlog value grew 43% to $6.12 billion, the highest second-quarter level in the Company’s history, with each of the Company’s four regions generating increases ranging from 18% in the West Coast to 98% in the Southeast. Ending backlog grew 23% to 12,331 homes.

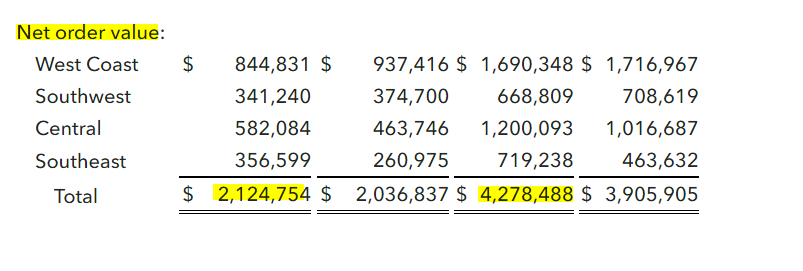

Net order value expanded by $87.9 million, or 4%, to $2.12 billion. Net orders of 3,914 decreased 9%, reflecting a moderation in monthly net orders per community to 6.2, compared to 7.0, partly offset by an increase in average community count.

The Company’s average community count increased 3% to 211, and ending community count increased 7% to 214.

The cancellation rate as a percentage of gross orders was 17%, compared to 9%.

기말 잔고 가치는 43% 증가한 61억 2,000만 달러로 회사 역사상 가장 높은 2분기 수준을 기록했으며, 회사의 4개 지역은 각각 서부 해안의 18%에서 남동부의 98%까지 증가했습니다. 기말 잔고는 23% 증가한 12,331가구였습니다.

순 주문 가치는 8,790만 달러(4%) 증가한 21억 2,000만 달러를 기록했습니다. 3,914개의 순 주문은 9% 감소했으며, 이는 커뮤니티당 월간 순 주문이 7.0에서 6.2로 조정되었음을 반영하며, 평균 커뮤니티 수의 증가로 부분적으로 상쇄되었습니다.

회사의 평균 커뮤니티 수는 3% 증가한 211개, 분기 종료시 커뮤니티 수는 7% 증가한 214개입니다.

총 주문 대비 취소율은 전년동기 9%에서 악화된 17%로 나타났습니다.

Balance Sheet as of May 31, 2022 (comparisons to November 30, 2021)

The Company had total liquidity of $925.6 million, with $244.2 million of cash and cash equivalents and $681.4 million of available capacity under its unsecured revolving credit facility.

Inventories grew 16% to $5.56 billion.

Investments in land acquisition and development for the six months ended May 31, 2022 increased 24% to $1.40 billion, compared to $1.13 billion for the year-earlier period.

The Company’s lots owned or under contract increased to 89,778, compared to 86,768. The lot pipeline has expanded 16% since May 31, 2021 as a result of the Company’s investments in land and land development over the past 12 months.

Of the Company’s total lots, approximately 58% were owned and 42% were under contract.

The Company’s 51,902 owned lots represented a supply of approximately 3.9 years, based on homes delivered in the trailing 12 months.

Notes payable increased by $400.2 million to $2.09 billion, reflecting borrowings outstanding under the unsecured revolving credit facility.

The Company’s debt to capital ratio was 38.8%, compared to 35.8%. The ratio was 37.7% at May 31, 2021.

On June 22, 2022, the Company completed the underwritten public offering of $350.0 million in aggregate principal amount of 7.25% senior notes due 2030 at 100% of their aggregate principal amount. The Company intends to use the net proceeds from the offering together with cash on hand, as needed, to retire its outstanding 7.5% senior notes due 2022 by redemption on July 7, 2022, pursuant to the optional redemption terms specified for such notes. In connection with this early extinguishment of debt, the Company expects to recognize a charge of approximately $4.0 million in the 2022 third quarter.

Stockholders’ equity expanded 9% to $3.29 billion, mainly reflecting strong net income growth.

On April 7, 2022, the Company’s board of directors authorized the Company to repurchase up to $300.0 million of its outstanding common stock. This authorization replaced a prior board of directors authorization. In the 2022 second quarter, the Company repurchased approximately 1.5 million shares of its outstanding common stock at a total cost of $50.0 million.

Book value per share of $37.76 increased 21% year over year.

회사의 총 유동성은 9억 2,560만 달러이며, 2억 4,420만 달러의 현금 및 현금성 자산과 6억 8,140만 달러의 무담보 회전 신용 편의를 보유하고 있습니다.

재고는 16% 증가한 55억 6,000만 달러를 기록했습니다.

2022년 5월 31일자로 종료된 6개월간 토지 취득 및 개발에 대한 투자는 14억 달러로 전년 동기의 11억 3000만 달러에 비해 24% 증가했습니다.

회사의 소유 또는 계약 중인 부지는 86,768에서 89,778로 증가했습니다. 부지 파이프라인은 지난 12개월 동안 토지 및 토지 개발에 대한 회사의 투자의 결과로 2021년 5월 31일 이후 16% 확장되었습니다. 회사의 전체 필지 중 약 58%가 소유되었고 42%가 계약 상태였습니다.

회사가 소유한 51,902개의 부지는 약 3.9년의 공급을 나타내며, 이는 후행 12개월 동안 인도된 주택을 기준으로 합니다.

미지급 어음은 무담보 회전 신용 편의에 따른 차입금을 반영하여 4억 200만 달러 증가한 20억 9000만 달러로 늘어났습니다.

회사의 자본 대비 부채 비율은 6개월전 35.8%에 비해 38.8%였습니다. 이 비율은 2021년 5월 31일에 37.7%였습니다.

2022년 6월 22일, 회사는 총 원금의 100%로 2030년 만기가 되는 7.25% 선순위 채권의 총 원금 총액 3억 5000만 달러의 인수 공모를 완료했습니다. 회사는 해당 어음에 대해 지정된 선택적 상환 조건에 따라 2022년 7월 7일 상환까지 2022년 만기 7.5% 선순위 채권을 소각하기 위해 필요에 따라 현금과 함께 공모의 순수익을 사용할 계획입니다. 이 부채의 조기 소멸과 관련하여 회사는 2022년 3분기에 약 400만 달러의 비용을 인식할 것으로 예상합니다.

주주 자본은 9% 증가한 32억9,000만 달러를 기록했는데, 주로 견조한 순이익 증가를 반영했습니다.

2022년 4월 7일, 회사의 이사회는 회사가 발행된 보통주 중 최대 3억 달러를 재매입할 수 있도록 허가했습니다. 이 승인은 이전 이사회 승인을 대체했습니다. 2022년 2분기에 회사는 약 150만주의 보통주를 총 5000만 달러에 재매입 했습니다. 주 당 장부 가치는 $37.76로 전년 대비 21% 증가했습니다.

Guidance(가이던스)

The Company is providing the following current guidance for its 2022 fiscal year(2022년)

Housing revenues(주택매출) in the range of $7.30 billion to $7.50 billion.

Average selling price(평균판매가격) will be approximately $500,000.

Homebuilding operating income(주택 영업이익)as a percentage of revenues in the range of 16.0% to 16.6%, assuming no inventory-related charges.

Housing gross profit margin(주택 매출총이익률) in the range of 25.6% to 26.2%, assuming no inventory-related charges.

Selling, general and administrative expenses(판관비) as a percentage of housing revenues in the range of 9.3% to 9.7%.

Effective tax rate(실효세율) of approximately 25%, assuming no federal energy tax credit extension is enacted.

Ending community count(커뮤니티 수) of approximately 250.

Return on equity(자기자본 이익률) in excess of 27%.

댓글