1.기업개요

About Steelcase Inc.

Organizations around the world trust Steelcase to help them create workplaces that help people work better, be inspired and accomplish more. The company designs, manufactures and partners with other leading organizations to provide architecture, furniture and technology solutions – accessible through a network of channels, including over 800 Steelcase dealer locations. Steelcase is a global, industry-leading and publicly traded company with fiscal 2022 revenue of $2.8 billion.

전 세계의 조직은 사람들이 더 잘 일하고 영감을 받고 더 많은 것을 성취할 수 있는 직장을 만드는 데 도움을 주는 Steelcase를 신뢰합니다. 이 회사는 아키텍처, 가구 및 기술 솔루션을 제공하기 위해 다른 주요 조직과 설계, 제조 및 파트 너 관계를 맺고 있습니다. 800개 이상의 스틸 케이스 딜러점을 포함한 채널 네트워크를 통해 액세스할 수 있습니다. Steelcase는 2022 회계연도에 28억 달러의 매출을 올린 글로벌, 업계 선도 기업이자 상장 기업입니다.

2.실적리뷰

실적을 리뷰하기전에 스틸케이스의 CEO인 Sara Armbruster의 발언을 보고 가겠습니다.

"We're pleased with our revenue growth of 33 percent, which was better than expected due to stronger incoming orders and improved order fulfillment from the adjustments we've made to mitigate the impact of supply chain disruptions," said Sara Armbruster, president and CEO. "In each of the most recent eight months of reported data, our year-over-year order growth in the Americas has outpaced our industry, and our EMEA segment has continued to deliver strong growth for the past five quarters."

공급망 중단의 영향을 완화하기 위해 수행한 조정으로 인해 주문의 수가 증가하고 주문 이행이 개선되어 예상보다 양호한 33%의 매출 성장을 달성한 것을 기쁘게 생각합니다. 최근 보고된 각 8개월 동안의 데이터에서 미주 지역의 연간 주문 증가율은 우리 업계를 앞질렀으며, EMEA 부문은 지난 5분기 동안 강력한 성장을 지속하고 있습니다.

"Inflationary pressures continued to grow this quarter across a number of commodities, and we responded by announcing our fifth price increase over the past 16 months, to be effective in July," said Dave Sylvester, senior vice president and CFO. "In addition, we recently announced a surcharge in the Americas in response to rapidly increasing costs of petroleum-based products, freight and delivery, and we have been slowing incremental spending to help offset some of the cost-price timing lag."

이번 분기에 여러 상품에 걸쳐 인플레이션 압력이 계속해서 증가했으며, 이에 대응하여 지난 16개월 동안 다섯 번째 가격 인상을 발표하여 7월부터 시행될 예정입니다. 또한 최근 석유 기반 제품, 화물 및 배송 비용이 급격히 증가함에 따라 미주 지역에서 추가 요금을 발표했으며 비용-가격 타이밍 지연을 일부 상쇄하는 데 도움이 되도록 점진적(증분) 지출을 늦추고 있습니다.

매출 : 740.7M

예측 : 690.94M(+7.2%)

EPS : -0.05

예측 : -0.182(+72.53%)

매출 및 주문의 강력한 성장에는 미주 및 EMEA 부문의 광범위한 강점이 포함됩니다.

상당한 인플레이션이 계속해서 결과에 영향을 미치면서 추가적인 가격 결정 조치를 취했습니다.

Halcon의 인수는 타협하지 않는 디자인과 장인 정신으로 성장 전략을 지원합니다.

2분기 전망은 인플레이션 압력 증가와 지속적인 공급망 문제에도 계절적 수익 개선을 예상합니다.

The revenue growth across all segments was driven by a strong beginning backlog and pricing benefits, as well as broad-based order growth in the Americas and EMEA. Revenue and order growth in the Other category was negatively impacted by COVID-related restrictions in China.

모든 부문의 매출 증가는 강력한 초기 백로그와 가격 혜택, 그리고 미주 및 EMEA의 광범위한 주문 증가에 의해 주도되었습니다. 기타 카테고리의 매출과 주문 증가는 중국의 코로나 관련 규제에 부정적인 영향을 받았습니다.

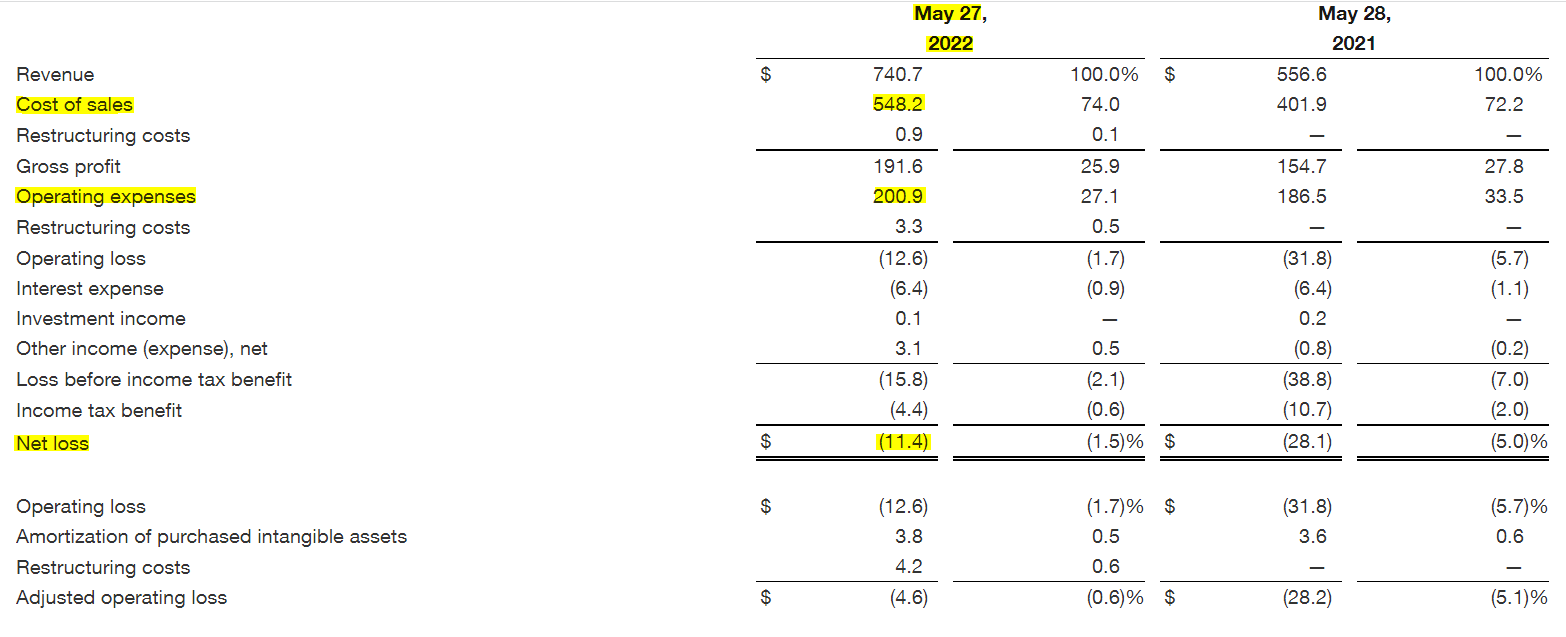

The year-over-year improvement in operating results was driven by the benefits of higher revenue, partially offset by lower gross margin. The current year included $4.2 million of restructuring costs in the Americas.

영업 결과의 전년 대비 개선은 매출 증가의 이점에 의해 주도되었으며 매출총이익률의 감소로 부분적으로 상쇄되었습니다. 현재 연도에는 420만 달러의 미주지역 구조 조정 비용이 포함되었습니다.

Gross margin of 25.9 percent in the first quarter represented a decrease of 190 basis points compared to the prior year, with a 270 basis point decline in the Americas, a 60 basis point decline in EMEA and a 100 basis point improvement in the Other category. The decline in the Americas was primarily due to approximately $15 million of higher inflation, net of pricing benefits, partially offset by the benefits of higher volume. The decline in EMEA was primarily due to unfavorable currency impacts and higher overhead costs, partially offset by the benefits of higher volume and approximately $4 million of higher pricing benefits, net of inflation. The improvement in the Other category was primarily due to the benefits of higher volume and lower overhead costs, partially offset by approximately $1 million of higher inflation, net of pricing benefits.

1분기 매출총이익률 25.9%는 전년도에 비해 190bp 감소했으며, 미주 지역은 270bp 하락, EMEA는 60bp 하락, 기타 카테고리는 100bp 개선됐다. 미주 지역의 하락은 주로 약 1,500만 달러의 높은 인플레이션으로 인한 것이며 가격 혜택을 제외하고 물량 증가의 혜택으로 부분적으로 상쇄되었습니다. EMEA의 하락은 주로 불리한 통화 영향과 높은 간접비로 인한 것이며, 인플레이션을 제외하고 물량 증가와 약 400만 달러의 높은 가격 혜택으로 부분적으로 상쇄되었습니다. 기타 카테고리의 개선은 주로 가격 혜택을 제외하고 약 100만 달러의 높은 인플레이션으로 부분적으로 상쇄된 더 많은 물량과 더 낮은 간접비의 혜택 때문이었습니다.

Operating expenses of $200.9 million in the first quarter represented an increase of $14.4 million, but a decline of 640 basis points as a percentage of revenue, compared to the prior year. The current year included $11.6 million of higher marketing, product development and sales expenses, $6.8 million of higher spending in other functional areas and $1.9 million from an acquisition, partially offset by a $4.0 million gain from the sale of land and $3.6 million of favorable currency translation effects.

1분기에 2억 90만 달러의 운영 비용은 1440만 달러가 증가했지만 수익 대비 640bp 감소했습니다. 올해에는 마케팅, 제품 개발 및 판매 비용 1,160만 달러, 기타 기능 분야에서의 지출 680만 달러, 인수로 인한 190만 달러가 포함되었는데, 이는 토지 매각으로 인한 400만 달러의 이득과 360만 달러의 유리한 통화 환산 효과로 일부 상쇄되었다.

Total liquidity, comprised of cash and cash equivalents and the cash surrender value of company-owned life insurance, aggregated to $279.5 million at the end of the first quarter. Total debt was $482.4 million. Adjusted EBITDA for the trailing four quarters was $151.6 million.

현금 및 현금성 자산과 회사 소유 생명 보험의 현금 상환 가치로 구성된 총 유동성은 1분기 말에 2억 7,950만 달러로 집계되었습니다.

The company completed the acquisition of Halcon Furniture LLC on June 10, 2022. The purchase price of $127.5 million, plus a $3.1 million adjustment for working capital, was funded from available cash and $68 million of borrowings under the company's global committed bank facility.

회사는 2022년 6월 10일에 Halcon Furniture LLC의 인수를 완료했습니다. 1억 2,750만 달러의 구매 가격과 운전자본 조정 310만 달러는 회사의 글로벌 약정 은행 편의(committed bank facility)에 따라 사용 가능한 현금과 6,800만 달러의 차입금으로 마련되었습니다.

The Board of Directors has declared a quarterly cash dividend of $0.145 per share, to be paid on or before July 18, 2022, to shareholders of record as of July 7, 2022.

Outlook(가이던스)

At the end of the first quarter, the company’s backlog of customer orders was approximately $927 million, which was 52 percent higher than the prior year. Consistent with recent quarters, the backlog includes a higher than historical percentage of orders scheduled to ship beyond the end of the next quarter, and supply chain disruptions are expected to continue. As a result, the company expects second quarter fiscal 2023 revenue to be in the range of $875 to $900 million. The company reported revenue of $724.8 million in the second quarter of fiscal 2022. The projected revenue translates to growth of 21 to 24 percent compared to the second quarter of fiscal 2022, or organic growth of 20 to 24 percent.

1분기 말에 회사의 고객 주문 잔고는 약 9억 2,700만 달러로 전년도보다 52% 증가했습니다. 최근 분기와 마찬가지로 백로그에는 다음 분기 말 이후에 배송될 예정인 주문의 비율이 역사적 비율보다 높으며 공급망 중단이 계속될 것으로 예상됩니다. 그 결과 회사는 2023 회계연도 2분기 매출이 8억 7500만~9억 달러 범위에 이를 것으로 예상하고 있습니다. 회사는 회 계연도 2022년 2분기에 7억 2,480만 달러의 매출을 보고했습니다. 예상 매출은 2022 회계연도 2분기 대비 21~24%의 성 장 또는 20~24%의 유기적 성장으로 해석됩니다.

The company expects to report earnings per share of between $0.06 to $0.10 for the second quarter of fiscal 2023 and adjusted earnings per share of between $0.11 to $0.15. The estimate includes:

회사는 2023 회계연도 2분기 주당 순이익을 0.06~0.10달러로 보고하고 조정 주당 순이익은 0.11~0.15달러로 예상하고 있다.

projected pricing benefits, net of inflation, of approximately $10 million as compared to the prior year

projected operating expenses of between $225 to $230 million

projected interest expense, investment income and other income, net, of approximately $4 million

a projected effective tax rate of 27 percent

예상 가격 혜택(인플레이션을 제외하고 전년도와 비교하여 약 1000만 달러)

2억 2500만 ~ 2억 3000만 달러의 예상 운영 비용

약 4백만 달러의 예상 이자 비용, 투자 수입 및 기타 수입

27%의 예상 실효 세율

The company reported earnings per share of $0.21 and had adjusted earnings per share of $0.23 in the prior year. The prior year included a $0.09 per share benefit related to a gain from the sale of land.

회사는 주당 순이익을 $0.21로 보고했으며 전년도에 조정 주당 순이익은 $0.23였습니다. 전년도에는 토지 판매 이익과 관련된 주당 $0.09의 혜택이 포함되었습니다.

“We continue to drive our strategy to lead the hybrid work transformation and prioritize investments to support our key growth adjacencies,” said Sara Armbruster. “At the same time, we remain committed to achieving our fiscal 2023 financial targets and are implementing necessary pricing actions and other measures to mitigate the impacts of the escalating inflationary pressures."

우리는 하이브리드 업무 혁신을 주도하기 위한 전략을 계속 추진하고 주요 성장 인접 요소를 지원하기 위한 투자 우선 순위를 정합니다. 우리는 2023 회계연도 재정 목표를 달성하기 위해 최선을 다하고 있으며 물가 상승 압력의 영향을 완화하기 위해 필요한 가격 책정 조치 및 기타 조치를 시행하고 있습니다.

댓글