1.기업개요

About Commercial Metals Company

Commercial Metals Company is a steel and metal manufacturer based in Irving, Texas.

In the United States, the company owns 41 scrap metal recycling facilities with a total annual capacity of 4.9 million tons, six electric arc furnace mini mills and two electric arc furnace micro mills and two re-rolling mills with a total annual capacity of 5.4 million tons, and steel fabrication facilities with a total annual capacity of 2.4 million tons. In Poland, it owns 12 scrap metal recycling facilities with a total annual capacity of 0.6 million tons, five steel fabrication facilities with a total annual capacity of 0.3 million tons, and a mini mill in Zawiercie with an annual capacity of 1.3 million tons.

Commercial Metals Company는 텍사스주 어빙에 위치한 철강 및 금속 제조업체입니다. 미국에는 연간 총 490만 톤의 고철 재활용 시설 41개, 전기로 미니 밀 6개, 전기로 마이크로 밀 2개, 총 연간 용량 540만 톤의 재압연 공장 2개 및 연간 총 240만 톤의 생산 능력을 갖춘 철강 제조 시설을 소유하고 있습니다. 폴란드에는 연간 총 용량 60만 톤의 고철 재활용 시설 12 개, 연간 총 용량 30만 톤의 철강 제조 시설 5개, Zawiercie에 연간 용량 130만 톤의 미니 밀을 소유하고 있습니다.

2.실적리뷰

실적을 리뷰하기전에 커머셜 메탈스의 CEO인 Barbara R. Smith의 발언을 보고 가겠습니다.

Barbara R. Smith, Chairman of the Board, President and Chief Executive Officer, said, "The third quarter was another remarkable financial result for our Company, underpinned by strong operational execution and robust market conditions across our key geographies. I am extremely proud of CMC's financial achievements during the quarter, especially in Europe. CMC employees in Poland have opened their homes and communities in a heartfelt grassroots effort to assist refugees fleeing the war in Ukraine. Amazingly, while responding to dire humanitarian needs, our team produced record quarterly adjusted EBITDA that nearly matched the best annual performance in the history of CMC's Europe segment."

3분기는 주요 지역에서 강력한 운영 실행과 견고한 시장 상황에 의해 뒷받침된 당사의 또 다른 놀라운 재무 결과였습니다. 저는 특히 유럽에서의 분기 동안 CMC의 재정적 성과를 매우 자랑스럽게 생각합니다. 폴란드의 CMC 직원들은 우크라이나 전쟁에서 탈출한 난민을 돕기 위한 진심 어린 노력의 일환으로 집과 지역사회를 개방했습니다. 놀랍게도 우리 팀은 심각한 인도주의적 필요에 대응하면서 CMC 유럽 부문 역사상 최고의 연간 실적과 거의 일치하는 기록적인 분기별 조정 EBITDA 를 만들었습니다.

Ms. Smith continued, "In late April, we welcomed Tensar to the CMC organization. Seeing the early results of the teams working together has only further reinforced our confidence in the strategic merits of this transaction and the potential for meaningful commercial synergies. With the onboarding of Tensar, CMC has added a highly attractive new growth platform and is creating a valuable and unique portfolio of solutions for existing and new markets."

4월 말, 우리는 CMC 조직에 Tensar를 맞이했습니다. 팀이 함께 작업한 초기 결과를 보면서 이 거래의 전략적 장점과 의미 있는 상업적 시너지 효과및 잠재력에 대한 확신이 더욱 강화되었습니다. Tensar의 온보딩으로 CMC는 매우 매력적인 새로운 성장 플랫폼을 추가했으며 기존 및 새로운 시장을 위한 가치 있고 고유한 솔루션 포트폴리오를 만들고 있습니다.

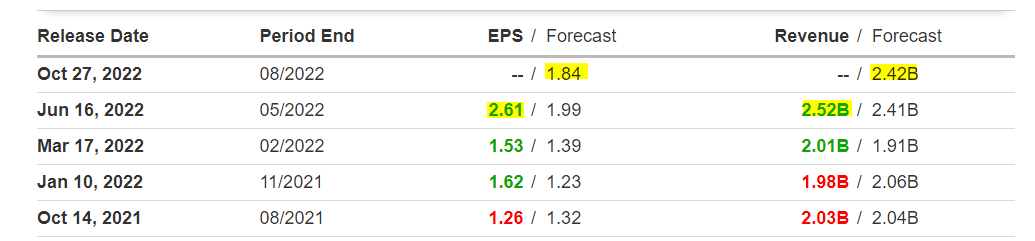

매출 : 2.52B

예측 : 2.41B(+4.56%)

EPS : 2.61

예측 : 1.99(+31.16%)

3억 1240만 달러 또는 희석 주당 2.54달러의 순이익은 전년도 기간의 1억 3040만 달러 또는 희석 주당 1.07달러에 비해 140% 증가했습니다.

4억 8,390만 달러의 핵심 EBITDA는 전년 대비 110% 증가했습니다. 지난 12개월 동안 총 14억 달러의 핵심 EBITDA 달성

북미와 유럽의 스크랩 대비 마진은 강한 시장 상황과 호의적인 고객 심리를 반영합니다.

볼륨 및 가격 기준으로 기록적인 입찰 활동 및 백로그 수준으로 북미 다운스트림 파이프라인의 지속적인 강점

Tensar Corporation 인수 완료, 새롭고 매력적인 전략적 성장 플랫폼 창출

The Company's balance sheet and liquidity position remained strong as of May 31, 2022. Cash and cash equivalents ended the quarter with a balance of $410.3 million, following a $550 million payment, net of cash acquired, to complete the purchase of Tensar. In addition, $624.3 million remained available under the Company's credit and accounts receivable facilities. CMC repurchased approximately one million shares of common stock during the quarter, returning $38.6 million of cash to shareholders. As of May 31, 2022, $294.4 million remained under the current share repurchase authorization.

회사의 대차대조표와 유동성 상태는 2022년 5월 31일 기준 강세를 유지하고 있습니다. 현금 및 현금성 자산은 Tensar 구매를 완료하기 위해 5억 5,000만 달러를 지불한 후 4억 1,030만 달러의 잔액으로 분기를 마감했습니다.(현금으로 구매) 또 한, 회사의 신용 및 매출채권 증권에 6억 2,430만 달러가 남아 있었습니다. CMC는 분기 동안 약 100만주의 보통주를 환매하여 주주들에게 3,860만 달러의 현금을 반환했습니다. 2022년 5월 31일 기준 2억 9440만 달러가 현재 주식 환매 승인에 남아 있습니다.

On June 15, 2022, the board of directors declared a quarterly dividend of $0.14 per share of CMC common stock payable to stockholders of record on June 29, 2022. The dividend to be paid on July 13, 2022, marks the 231st consecutive quarterly payment by the Company, and represents a 17% increase from the dividend paid in July 2021.

Business Segments - Fiscal Third Quarter 2022 Review(부문별 결과)

Demand for CMC's finished steel products in North America was again robust during the quarter, with several key internal and external indicators pointing toward continued strength. Downstream bid volumes, a key indicator of the construction project pipeline, increased meaningfully from a year ago, resulting in the expansion of contract backlog levels. Demand from industrial end markets continued to trend positively, with most end use applications increasing compared to the prior year period.

북미에서 CMC의 철강 완제품에 대한 수요는 분기 동안 다시 강세를 보였고 여러 주요 내부 및 외부 지표가 지속적인 강세를 나타냈습니다. 건설 프로젝트 파이프라인의 핵심 지표인 다운스트림 입찰 물량이 1년 전에 비해 의미 있게 증가하여 계약 잔고 수준이 확대되었습니다. 산업용 최종 시장의 수요는 계속해서 긍정적인 추세를 보였고 대부분의 최종 사용 애플리케이션은 전년도 기간에 비해 증가했습니다.

The North America segment reported adjusted EBITDA of $379.4 million for the third quarter of fiscal 2022, an increase of 83% compared to $207.3 million in the prior year period. This improvement was driven by record margins on sales of both steel products and raw materials. Steel products have experienced five consecutive quarters of year-over-year margin expansion, while margins on raw material sales have grown for nine consecutive quarters. Controllable costs per ton of finished steel shipped were unchanged in comparison to the second fiscal quarter, but were up from the prior year period primarily as a result of higher per unit purchase costs for freight, energy and alloys.

북미 부문은 2022 회계연도 3분기 조정 EBITDA가 3억 7,940만 달러로 전년 동기의 2억 730만 달러에 비해 83% 증가했다고 보고했습니다. 이 같은 개선은 철강제품과 원자재 판매량 모두 사상 최대 마진을 기록한 데 따른 것입니다. 철강 제품은 5분기 연속 전년 대비 마진 확대를 경험했으며, 원자재 판매 마진은 9분기 연속 증가했습니다. 선적된 완제품 철강 톤당 통제 가능한 비용은 2분기와 비교하여 변동이 없었지만 주로 화물, 에너지 및 합금에 대한 단위당 구매 비용이 증가한 결과 전년도 기간보다 증가했습니다.

Shipment volumes of finished steel, which include steel products and downstream products, followed typical seasonal patterns, and were essentially unchanged from the prior year period. The average selling price for steel products increased by $316 per ton compared to the third quarter of fiscal 2021, while the cost of scrap utilized rose $103 per ton. The result was a year-over-year increase of $213 per ton in margin over scrap. The average selling price for downstream products increased by $281 per ton from the prior year period and $75 per ton on a sequential basis. Future pricing indicators on new work entering the backlog remain positive, as average price levels for bids and new awards climbed significantly from the prior year period.

철강제품과 다운스트림 제품을 포함한 철강 완제품의 출하량은 전형적인 계절적 패턴을 따랐으며, 본질적으로 전년도 기간과 변동이 없었습니다. 철강제품의 평균 판매가격은 2021회계연도 3분기에 비해 톤당 316달러 증가한 반면, 스크랩 이용 원가는 톤당 103달러 상승했습니다. 그 결과 스크랩 대비 마진이 톤당 $213 증가했습니다. 다운스트림 제품의 평균 판매 가격은 전년도 기간보다 톤당 $281, 직전분기 보다 톤당 $75 증가했습니다. 입찰 및 신규 낙찰에 대한 평균 가격 수준이 전년도 기간보다 크게 상승함에 따라 백로그에 들어가는 신규 작업에 대한 미래 가격 지표는 긍정적인 상태를 유지합니다.

The Europe segment reported record adjusted EBITDA of $121.0 million for the third quarter of fiscal 2022, up 142% compared to adjusted EBITDA of $50.0 million for the prior year quarter. The improvement was driven by a significant expansion in both shipment volume and margin over scrap. Similar to North America, underlying demand for steel products remained robust. Volumes of rebar, merchant bar, and wire rod increased on a year-over-year basis, assisted by the addition of a third rolling line, which improved production flexibility and the mill's ability to capitalize on favorable market conditions. During the first 12 months of operating the new rolling line, quarterly shipment volumes of finished products have increased 35% compared to the average of the preceding five years.

유럽 부문은 2022 회계연도 3분기 조정 EBITDA가 1억 2100만 달러로 전년 동기 5000만 달러에 비해 142% 증가했다고 보고했다. 이러한 개선은 출하량과 스크랩에 대한 마진이 크게 확대되었기 때문입니다. 북미와 유사하게 철강 제품에 대한 기본 수요는 견조한 상태를 유지했습니다. 철근, 머천트 바 및 선재의 양은 생산 유연성을 개선하고 유리한 시장 조건을 활용하는 공장의 능력을 개선한 세 번째 압연 라인의 추가로 인해 전년 대비 증가했습니다. 신규 압연 라인을 가동한 첫 12개월 동안 완제품의 분기별 출하량은 이전 5년 평균에 비해 35% 증가했습니다.

As a result of continued strong demand and constrained supply in the wake of trade sanctions against Russia and Belarus, average selling price increased by $303 per ton compared to the prior year quarter, while the cost of scrap utilized rose $154 per ton. The result was a year-over-year increase in margin over scrap of $149 per ton.

러시아 및 벨라루스에 대한 무역 제재로 인한 수요 증가와 공급 제한의 결과 평균 판매 가격은 전년도 분기에 비해 톤당 $303 증가했으며 스크랩 활용 비용은 톤당 $154 증가했습니다. 그 결과 톤당 $149의 스크랩 대비 마진이 전년 대비 증가했습니다.

The Company's new Tensar business generated EBITDA of $4.9 million during its first five weeks as part of CMC. Excluding a $2.2 million charge to reflect purchasing accounting effect on inventory, EBITDA amounted to $7.1 million on net sales of $28.0 million. EBITDA margin of 25.4% was consistent with Tensar's trailing five-year average. Tensar's financial performance is included within CMC's existing operating segments, with North American results incorporated into CMC's North America segment and all other operations included in the Europe segment.

회사의 새로운 Tensar 사업은 CMC의 일부로 처음 5주 동안 490만 달러의 EBITDA를 생성했습니다. 재고에 대한 구매 회계 효과를 반영하기 위한 220만 달러 비용을 제외하고 EBITDA는 2800만 달러의 순매출에서 710만 달러에 달했습니다. 25.4%의 EBITDA 마진은 Tensar의 후행 5년 평균과 일치했습니다. Tensar의 재무 성과는 CMC의 기존 운영 부문에 포함되며 북미 지역 결과는 CMC의 북미 부문에 통합되고 기타 모든 운영은 유럽 부문에 포함됩니다.

Outlook(가이던스)

Ms. Smith said, "We anticipate strong financial performance to continue in the fourth quarter. Robust demand for each of CMC's major product lines is expected to persist, augmented by our growing downstream backlog and solid levels of new work entering the project pipeline. Margins over scrap in both North America and Europe should remain at levels near those of the third quarter, driven by favorable market conditions across our geographies."

4분기에도 강력한 재무 실적이 계속될 것으로 예상합니다. CMC의 각 주요 제품 라인에 대한 강력한 수요는 다운스트림 백로그 증가와 프로젝트 파이프라인에 들어가는 견고한 수준의 신규 작업으로 인해 계속될 것으로 예상됩니다. 북미와 유럽 모두에서 스크랩에 대한 마진은 우리 지역 전반에 걸쳐 유리한 시장 상황에 힘입어 3분기 수준에 머물 것입니다.

Ms. Smith added, "Looking into CMC's fiscal 2023, we see several factors that should support continued strength in construction markets. Firstly, as a result of the continued high levels of new bidding activity, we anticipate entering our new fiscal year with historically high levels of contract backlog. In addition, new project bid levels should remain strong based on the benefits of rising activity related to the recently enacted federal infrastructure bill, non-residential construction activity supported by follow-on investment in the wake of historically high new residential community formation in our home markets, and from the continuation of reshoring trends that have already resulted in significant new projects. The expected early calendar 2023 startup of our Arizona 2 micro mill will provide CMC with a greater flexibility to capitalize on these anticipated favorable demand conditions."

CMC의 2023 회계연도를 살펴보면 건설 시장의 지속적인 강세를 뒷받침해야 하는 몇 가지 요소가 있습니다. 첫째, 계속 높은 수준의 신규 입찰 활동의 결과로 우리는 역사적으로 높은 수준의 계약 잔고로 새 회계 연도에 진입할 것으로 예상합니 다. 또한, 신규 프로젝트 입찰 수준은 최근 제정된 연방 기반 시설 법안과 관련된 증가하는 활동의 이점을 기반으로 하여 강력하게 유지되어야 하며, 우리 국내 시장에서 역사적으로 높은 신규 주거 커뮤니티 형성에 따른 후속 투자로 지원되는 비주거 건설 활동과 이미 상당한 새 프로젝트로 이어진 리쇼어링 추세의 지속이 뒷받침되어야 합니다. 2023년 초 예상되는 Arizona 2 마이크로 밀의 시작은 CMC에 이러한 예상되는 유리한 수요 조건을 활용할 수 있는 더 큰 유연성을 제공할 것입니다.

댓글